404

Page not found

Page not found

Victor Hugo once wrote that “Nothing is so powerful as an idea whose time has come”. Recognising the true value of natural capital, is one such idea. Across private and public sectors, across disciplines, and around the world, initiatives to advance and develop natural capital thinking have emerged rapidly over the past 10 years.

In a blizzard of acronyms, we have the NCC, SEEA, WAVES, IIRC, KIP-INCA, A4S, GRI, EO4EA – among many others. Are they the same, are they competing, are they useful? To both insiders and outsiders this range of initiatives is confusing at best. At worst, it leads to a lack of engagement, avoidance and misunderstanding.

The reality is that, while differences among these various initiatives do exist, they have all been motivated by a common understanding of the reality that we are losing our stocks of natural capital – and that this matters.

While each initiative may have different origins, some differing objectives, and may reflect variations in technique and method, there is much common ground. Indeed, to engage the broader community in tackling the natural capital challenges we collectively face, we cannot afford to focus on distinctions. Instead, we must look to build on the overlaps and seek to build a common language that will enable the exchange of ideas and ongoing innovation.

It is in this spirit of collaboration that the Natural Capital Coalition, together with the IDEEA Group and supported by over 20 organisations, launches this statement on Combining Forces on Natural Capital.

It is especially relevant that this statement of collaboration is launched at the World Forum on Natural Capital, where leading voices in the movement gather every two years, to share best practice, enduring challenges and build further collaborations.

While progress to date has largely taken place in small pockets, in order to move forward we need to ramp up our efforts and move beyond talking with supporters and “the converted”.

For this, we need leaders who can establish spaces for dialogue and development, and who can ensure that technical debates do not form a barrier to progress, that we take full advantage of the diversity of skills and experience already engaged, and that the big picture is always kept in mind.

I encourage you to take the opportunity to read the statement, to share it within your organisations, to sign on, and to join us as we move towards a better understanding and appreciation of the complex and beautiful world in which we live.

Carl Obst is Director of the Institute for the Development of Environmental-Economic Accounting (IDEEA Group), and Lead Author of the United Nation’s System of Environmental-Economic Accounting (UN SEEA).

You can join the Coalition as an individual or as an organization

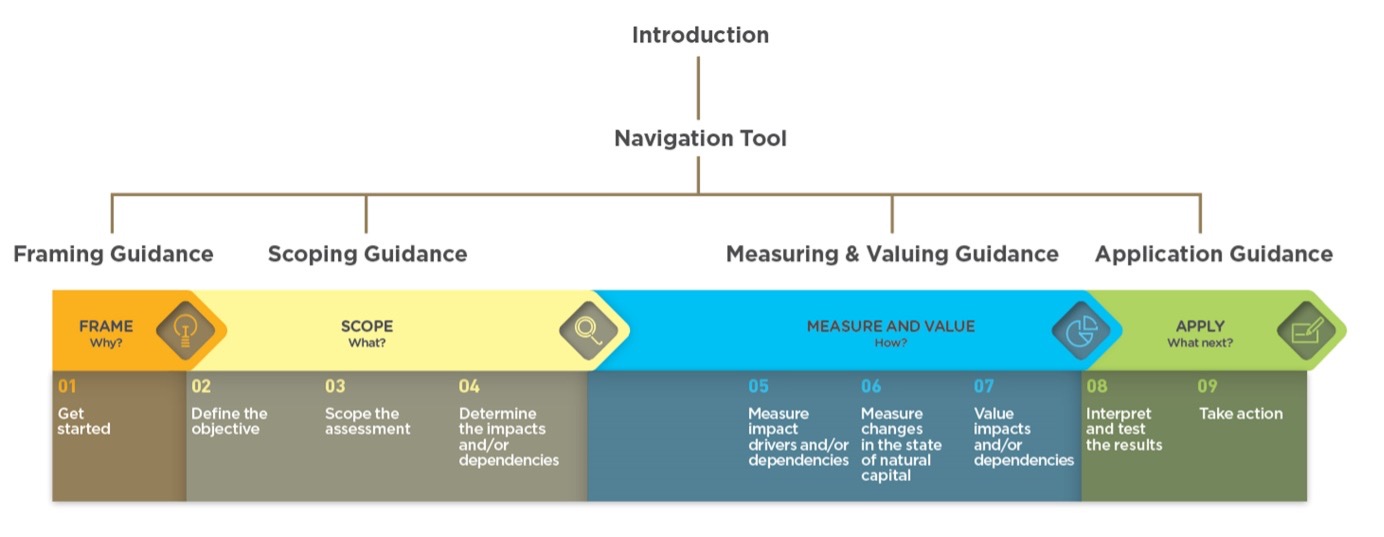

Developed by the Capitals Coalition and UNEP-WCMC, the Navigation Tool compliments the Biodiversity Guidance by steering practitioners through a series of interactive questions to help them undertake a biodiversity-inclusive natural capital assessment. The tool also offers supporting resources, tools, methodologies and advice to assist an assessment based on user responses.

Biodiversity constitutes the living component of natural capital and underpins the success of businesses around the world. But the benefit that biodiversity provides to organizations can be hard to fully understand, and even harder to effectively measure and value.

The Cambridge Conservation Initiative and Capitals Coalition developed the Biodiversity Guidance to accompany the Natural Capital Protocol. It is designed to help businesses and financial institutions to better understand the value they receive from biodiversity, and to apply this knowledge as they make decisions, through a biodiversity-inclusive natural capital assessment.

The Navigation Tool questions are tied to the stages and steps in the Natural Capital Protocol and guide users through the Frame, Scope, Measure & Value and Apply stages that constitute a natural capital assessment.

Two primers accompany the Biodiversity Guidance and Navigation Tool. They set out the value that organizations will receive from carrying out an assessment, and an overview of how to conduct the assessment .